Secured Smart Bank and Financial Institutions long tern Sustained Growth strategies through Industrial HUBs

By Mr. Sai Prasath

A Global Financial Specialist

By Aditya Sekhar

CEO & Chairman Micro Media Marketing PVT Ltd., Smart City Scholar

India & Its Banking Growth… a perspective

In the modern’s economic system, banks play a very important role in economic development of country. They collect the surplus savings of the people and make them available for investment. They also create new demand deposits in the process of granting loans and purchasing investment securities. They facilitate trade both inside and outside the country. Commercial banks are an important part of the financial system of the country.

The present Indian banking system consists of 18 public sector banks, 22 private sector banks, 46 foreign banks, 53 regional rural banks, 1,542 urban cooperative banks and 94,384 rural cooperative banks are providing financial services in all segments of the society.

Modern banking in India originated in the last decade of the 18th century. Among the first banks were the Bank of Hindustan, which was established in 1770 and liquidated in 1829–32; and the General Bank of India, established in 1786 but failed in 1791.

The largest and the oldest bank which is still in existence is the State Bank of India (SBI). It originated and started working as the Bank of Calcutta in mid-June 1806. In 1809, it was renamed as the Bank of Bengal. This was one of the three banks founded by Presidency Government; the other two were the Bank of Bombay in 1840 and the Bank of Madras in 1843. The three banks were merged in 1921 to form the Imperial Bank of India, which upon India’s independence, became the State Bank of India in 1955. For many years the presidency banks had acted as quasi-central banks, as did their successors, until the Reserve Bank of India was established in 1935, under the Reserve Bank of India Act 1934.

In 1960, the State Banks of India was given control of eight state-associated banks under the State Bank of India (Subsidiary Banks) Act, 1959. These are now called its associate Banks. In 1969 the Indian Government Nationalized 14 major private banks; one of the big banks was Bank of India. In 1980, 6 more private banks were nationalized. These nationalized banks are the majority of lenders in the Indian Economy. They dominate the banking sector because of their large size and widespread networks.

The Indian banking sector is broadly classified into scheduled and non-scheduled banks. The scheduled banks are those included under the 2nd Schedule of the Reserve Bank of India Act, 1934. The scheduled banks are further classified into: nationalized banks; State Bank of India and its associates; Regional Rural Banks (RRBs); foreign banks; and other Indian private sector banks. The term commercial banks refer to both scheduled and non-scheduled commercial banks regulated under the Banking Regulation Act 1949.

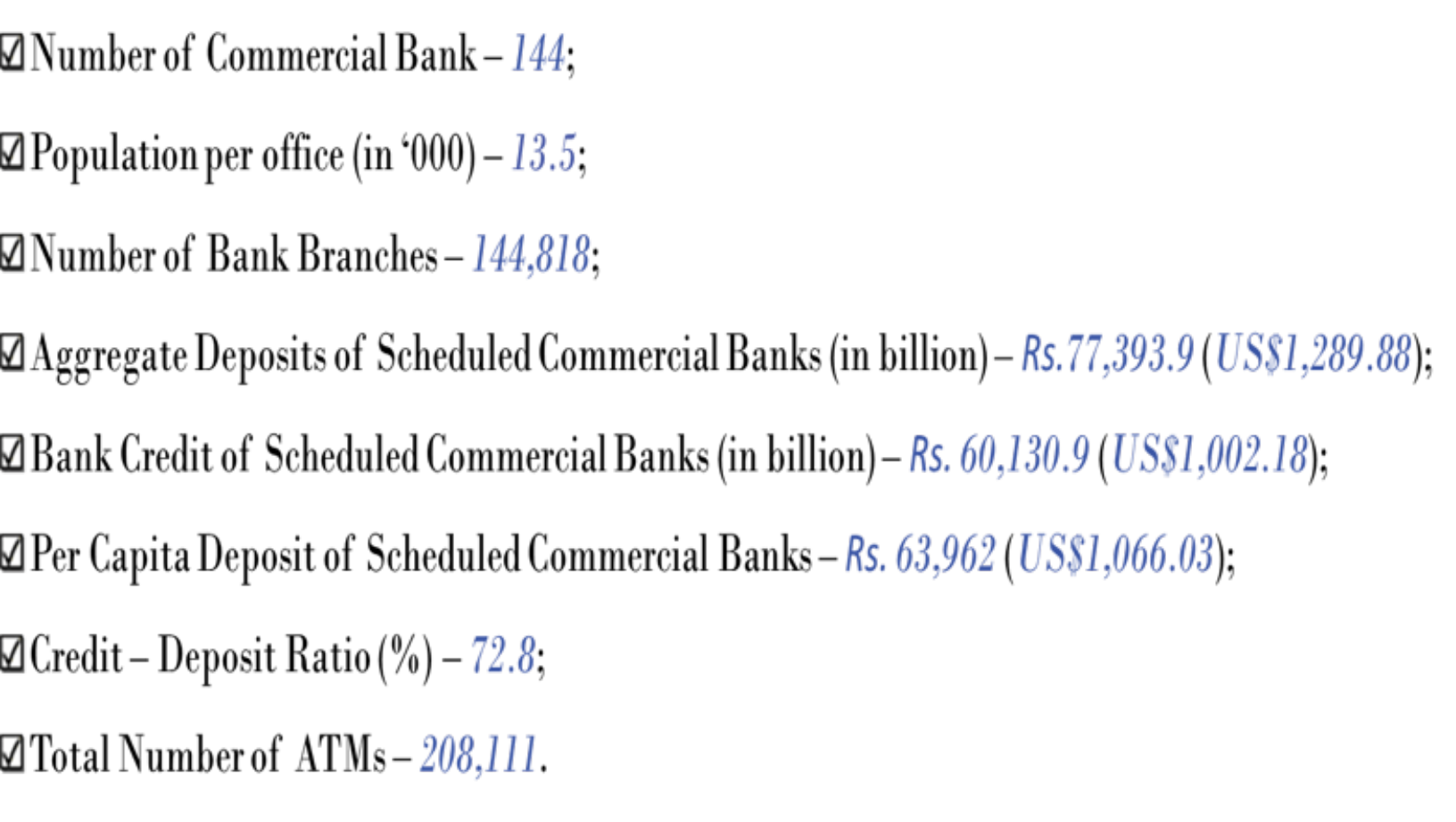

Banking in India — Key Indicators

Payment Bank

Payments Bank is a new model of banks conceptualized by the Reserve Bank of India (RBI). These banks can accept a restricted deposit, which is currently limited to One lakh rupees per customer. These banks may not issue loans or credit cards but may offer both current and savings accounts. Payments banks may issue ATM and debit cards and offer net-banking and mobile-banking. The banks will be licensed as payments banks under Section 22 of the Banking Regulation Act 1949, and will be registered as Public Listed Company under the Companies Act 2013.

Small finance Banks

To further the objective of financial inclusion, the RBI granted approval to ten entities to set up small finance banks. Since then, all ten have received the necessary licenses. A small finance bank is a niche type of bank to cater to the needs of people who traditionally have not used scheduled banks. Each of these banks is to open at least 25% of its branches in areas that do not have any other bank branches (unbanked regions). A small finance bank should hold 75% of its net credits in loans to firms in priority sector lending, and 50% of the loans in its portfolio must be less than INR. 25 lakh (US$38,000).

Indian Banking Industry - Government Initiatives

- • As per Union Budget 2019-20, the government has proposed fully automated GST refund module and an electronic invoice system that will eliminate the need for a separate e-way bill.

- • Under the Budget 2019-20, government has proposed INR. 70,000 crore (US$10.2 billion) to the public sector bank.

- • Government has smoothly carried out consolidation, reducing the number of Public Sector Banks by eight.

- • The Government of India has made the Pradhan Mantri Jan Dhan Yojana (PMJDY) scheme an open ended scheme and has also added more incentives.

The Government of India is planning to inject INR. 42,000 crore (US$ 5.99 billion) in the public sector banks by current financial year and will infuse the next tranche of recapitalization by mid of the financial year.

Indian Banking Industry - Achievements

Following are the achievements of the government in the Indian Banking Industry:

- • Last year the number of debit and credit cards issued were 925 million and 47 million, respectively.

- • As per RBI, the present, India recorded foreign exchange reserves of approximately US$ 442.58 billion.

- • India ranks among the top seventh economies with a GDP of US$ 2,73 trillion in current year and economy is forecasted to grow at 7.3% in coming year.

- • To improve infrastructure in villages, 204,000 Point of Sale (PoS) terminals have been sanctioned from the Financial Inclusion Fund by National Bank for Agriculture & Rural Development (NABARD).

- • The number of total bank accounts opened under Pradhan Mantri Jan Dhan Yojana (PMJDY) reached 333.8 million at present year.

Indian Banking Industry - Road Ahead

Enhanced spending on infrastructure, speedy implementation of projects and continuation of reforms are expected to provide further impetus to growth. All these factors suggest that India’s banking sector is also poised for robust growth as the rapidly growing business would turn to banks for their credit needs.

Also, the advancements in technology have brought the mobile and internet banking services to the fore. The banking sector is laying greater emphasis on providing improved services to their clients and also upgrading their technology infrastructure, in order to enhance the customer’s overall experience as well as give banks a competitive edge.

India’s digital lending stood at US$75 billion in last financial year and is estimated to reach US$1 trillion by FY2023 driven by the five-fold increase in the digital disbursements.

The Concept of Secured Governance into the Banking Industry

Secured Governance offers a strategically initiative by the Government for the Government to enhance the spending’s on basic infrastructure development with a minimal investment by the respective Banks. It is a concept of developing Techno Economic Corridors connecting hubs which will act as growth centre for individual sectors. The very concept of “Secured’’ here implies a secured convergence or knitting with various sectors defining a growth for an economy.”

Advantages of the Proposed participation of Banking Industry in the Secured Governance

- • Secured governance initiatives acts as a catalyst for improvising the effective Infrastructure across India as well reducing Non-performing assets (NPAs) in banking sector drastically through our uleashing National Growth of business. The Value proposition of the proposed banking HUB under SG initiatives tends to grows many folds.

- • Banking HUB under SG - A cluster been created in a concentrated city or rural area In India, that is considered to be a focal point for the Banking & Financial associated services along with many Integrated Commercial Developments. Synergy, or the potential financial benefit achieved through the combining of banking sector with industries. The Special Purpose Vehicle (SPV) becomes an indirect source of financing for banks by attracting independent equity investors to augment their debt obligations.

- • These HUBs are home to all type of public & private industries and enterprises. The financial services coupled with commercial establishments will be provided under the various initiatives of the banking industry to all business enterprises.

- • Banks could provide loans to public and private industries for investment in infrastructure development of the proposed Banking HUB.

- • The banking industry could also facilitate an exclusive CA, CPA, Legal, Management services such as auditing, bookkeeping, payroll processing, and tax return preparation from these HUB developments, so as to have the Integrated HUB development on par with International Integrated Commercial centers.

- • The proposed Banking HUB development initiatives across India shall be running in concurrence with the Govt. of India’s Global Smart City Initiatives across 120 Cites in India.

- • The proposed Banking HUB would also setup to facilitate OBU (offshore Banking unit) Free trade Zone under its International Financial Center (as Special Economic Zone in India) offers loans in the Multi currencies as well accept deposits from foreign banks and other OBUs.

- • The proposed Banking HUB would eventually facilitate the best of REIT (real estate Investment trust) growth prospects in India by which the real estate in India would grow multi fold with greater International Investments attraction.

- • The proposed Banking HUB initiatives could facilitate and improvise the SME & MSME sectors in India due to its various cluster developments with a lesser burden on infrastructure Investment Cost by the Industry owners across India.

Comments

Vishal P

July 10, 2016 AT 9:15 PM

Vishal P

July 10, 2016 AT 9:15 PM

Leave A Comment